So you’ve just finished university with a maxed out overdraft, no hope of getting all of your last house deposit back, and months until your first graduate role payday. I promise you are not alone in not knowing what the hell you’re going to do to get your finances in order.

I have been hyper-independent for as long as I remember and I think that might be the reason why I have always been deemed responsible with my money. But really I’m just privileged enough to be able to ask family for financial support if ever necessary, but too stubborn and proud to ever do so. I know this is not the case for everyone and I also know that figuring out the best thing to do with the precious little money you earn can feel like a minefield. So, on the requests of friends, I’ve created this step-by-step guide to hold your hand on the journey to financial responsibility. I honestly believe we all deserve to work and live without stressing about money, and I know this seems less and less attainable these days, but I’m hoping with this guide you’ll be able to get there.

Strategy

I budget thinking about my financial future and goals ie. home ownership, retirement while also prioritising enjoying my life. These house deposits and pension pots are long term investments which benefit from the length of time they are held for. £100 invested 10 years before retirement is significantly less valuable than £100 invested 40 years before retirement. I tried to calculate the difference, but decided you should just trust me instead.

Its a fairly safe assumption that as we get older our income will increase. I also think its fair for us to want to be paid more as our experience grows. So my strategy with my finances takes this into account.

- Balance saving early on for longer term benefits, with rewarding yourself in the short term – Save money to spend on travelling and having fun while your young too

- Benefit from time as much as possible by investing heavily in your pension in your early 20’s – before your expenses increase through home ownership or having a family

- Minimise the psychological challenge of saving money – pay into your pension ASAP, and send savings out of your current account as soon as you get payed so you never feel like you’ve missed out on spending them

Pensions

If you are working, you should contribute to a pension. Check the maximum percentage of income your employer will match and make this the minimum you contribute. You can use calculators online to suggest what you should put into your pension, but a general rule of thumb I use is to aim for total contributions to be 15% of your income.

Great Example: Your maximum employer contribution is 6%. Therefore, if you contribute 9% your total contributions will be 15%.

Good Example: Your employers maximum contribution is 6% so you contribute 6%. Your employer matches this making your total contribution 12%

Less-than-ideal Example: Your employers maximum contribution is 6%, but you only contribute 4%. Your employer matches this making your total contribution 8%.

Pensions Q&A

Q: What’s the point of paying into a pension when they keep raising the retirement age?

A: The retirement age you’re referring to is the state retirement age. This dictates how old you have to be to stop working and receive your state pension. It is currently 67 years old however this is expected to continue to rise steadily. Your workplace pension scheme has its own age at which you can access your investment, usually between 60 and 65.

Q: Why do I need to pay into a workplace pension if I have a state pension?

A: Yes, you pay national insurance which in part goes towards your state pension. I’ve mentioned above that this is usually accessible later than your workplace pension is. However, its also worth noting that those who are entitled to a full state pension are currently only receiving £11,502 per year. Workplace pensions add to this, to create a liveable income during retirement.

Q: Why should my contributions be at least the maximum my employer will match?

A: Because if you’re not matching your employers maximum contribution you are missing out on free money! You might think you benefit now by paying less into your pension and more into your current account. But a deduction in your pension contribution of just 1% if you’re earning £27,000 is just £22 a month after tax. This could have instead been £45 in your pension pot, which after 40 years invested could have been over £2000. I think the numbers speak for themselves.

Q: How can I change my contributions?

A: Most work places will give you the last month of their financial year to change your workplace benefits and salary sacrifices. If you’re not sure when this is or how to do this, speak to your manager or HR.

Budgeting

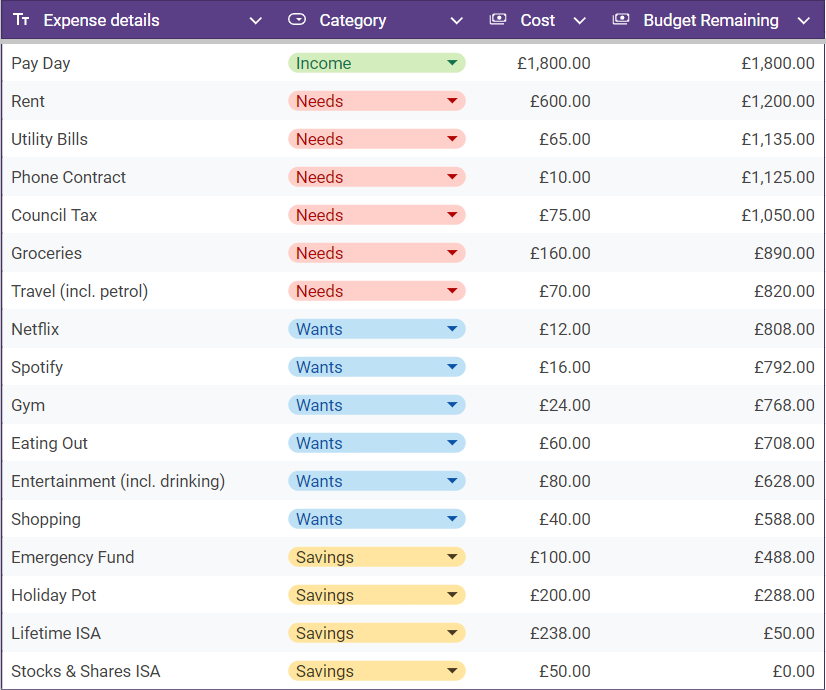

Most guidance online recommends the 50/30/20 rule. This is where 50% of your income (or less) is spent on needs, 30% on wants, and 20% on savings/investments. This could be helpful if you’re not sure what you can afford say if you’re relocating and looking for somewhere to rent. Its important to live within your means and housing is a massive outgoing expense each month. If you can, aim to spend a third of your income or less on rent. I completely understand that this is increasingly difficult in the current rental market in the UK. But it still may be a helpful guideline as to what you can afford comfortably.

To create your monthly budget, first list all of your needs. This means rent, bills, petrol, travel passes, average grocery costs.

Calculate what’s leftover from your income after your needs are taken care of. In an ideal world we should then allocate that money to each of the following, before taking a portion for wants.

- Debt (eg. student overdraft)

- Emergency Fund (3-6 months needs)

- Lifetime ISA (house deposit)

- Specific Savings Pots (eg. holiday, new car, tattoo)

- Invest

I said ideal world. So, realistically what you’re going to do is save a little money each month into your specific savings pots so you can enjoy life (not just work yourself to the bone) and work down that list in order of priority. Everybody wants to invest these days, but until you’re saving the maximum you can in a Lifetime ISA (£333 per month) I want you to forget about it. Why? Scroll down to read more about Lifetime ISA’s.

Once you have your budget planned, set up standing orders for your savings at the start of the month so you’re not tempted to touch that money. It can be useful to have more than one current account, for example a brick and mortar bank like Santander, Lloyds, Nationwide aswell as a new style bank like Monzo, Starling, Revolut. I have my banking set up so I get payed into my traditional current account and all my set expenses (most of my needs) come out of there by direct debit. I have a standing order set-up to transfer money for any of my variable spending (mostly my wants) into my Monzo, which then allows me to track how well I stick to my budget.

If you find yourself consistently unable to stick to your budget, cut yourself some slack and adjust your targets to be more attainable. So much of being good with money is understanding our mindset and psychology around it. Yes we want to save for our future, but you also need to feel rewarded for the work you are doing right now. It is much better to plan some spending to treat yourself each month, than set an unattainable budget that you constantly ignore.

Student Overdrafts

Most student overdrafts will offer 0% interest for 1-2 years after you finished your course. So why should we pay this off as soon as possible? Because not paying off overdrafts in a timely manner, even when they are arranged overdrafts like student overdrafts are, will negatively impact your credit score. I personally kept my graduate account with its arranged overdraft for as long as I could, just in case of emergencies. But if you think it would be more beneficial for you to switch current account after paying off any overdraft then go for it!

Emergency Fund

In case of unexpected costs, or loss of income, its important to have an emergency fund which is readily accessible for example in a Cash ISA. A good goal to set, is for your emergency fund to cover 6 months of your needs. If you’re on a graduate scheme, you might aim to reach this goal by the end of your 2 year scheme, if not sooner. How do you figure out how much you should save each month for this? In my example budget my needs are around £1000 so I would aim for my emergency fund to be £3000 for 3 months. £3000 divided by the 24 months spent on a 2 year grad scheme is £125. So I would save a minimum of £125 ideally into my emergency fund each month.

Lifetime ISA

A Lifetime ISA is a type of tax-free savings account. Each year you can deposit a maximum of £4,000 into Lifetime ISA’s and benefit from a 25% bonus from the government on your deposits. This means that if you make full use of your Lifetime ISA allowance you with be awarded £1000 each year, with interest calculated on top of this. You forfeit this government bonus if you make any withdraws that are not to purchase your first home, or as a pension. You might see this described as a 25% penalty for withdrawals.

Specific Savings Pots

For short term savings goals I utilise savings pots in Monzo. Alternatively you could open a seperate Easy Access Savings Account or Cash ISA for each of your short term savings goals. Like with your emergency fund, you can decide how much you want to save for these goals each month by setting a savings goal and date then dividing the goal by the number of months you have to save.

Longer term savings (1-3 years) might be better off in a Fixed Rate ISA. Fixed Rate ISA’s provide a fixed interest rate (as opposed to variable) for a certain number of years. They tend to have penalties associated with withdrawing money before the end of that fixed term.

A lower commitment option to a fixed rate account is a 90 day access account. Like it says on the tin, it takes 90 days from when you request a withdrawal to receive it from one of these accounts without incurring penalties.

Those both sound really inconvenient right? They can be, but dependent on what interest rates are doing, they can offer significantly more interest on your savings than easy access accounts. Honestly, it can be a gamble because you could end up with a fixed rate account that starts at a higher interest rate but end up significantly lower by the end of the fixed term. This is why I wouldn’t consider them unless the interest rates offered are at least 2% higher than easy access alternatives.

Investments

If you have long term savings goals of 5-10 years that isn’t your first house deposit you would benefit from investing your savings instead of using Saving Accounts or Cash/Fixed Rate ISA’s. Why do I say this? Any money you invest is at risk. This means that you could lose it. But speaking generally, overtime changes in interest rates and the stock market means that mixed investments (investments of various stocks, shares and bonds) should always increase in value. The longer you leave your money invested, the more likely you are to benefit from these changes. Most advice recommends investing with the expectation to not see returns for 5-10 years.

There are multiple ways to start investing, some requiring a fair amount of research and some that don’t. You do not need a background in finance or to be super intelligent to invest successfully, but some methods will require a greater time and energy investment to see success. This is why I have personally only ever invested via robo-investment platforms. These platforms do all the research for you, charging you a management fee for their insight. Some platforms will offer more pro-active management for a greater management fee. This means they will alter your investments in response to the market more regularly. Robo-investment platforms assess your appetite for risk (how ok you are with losing the money you plan to invest) and suggest a risk level for you to invest at. You must have £500 ready to invest to open an account with most robo-investment platforms.

If you do want to start investing, make sure you are using your £20,000/year ISA allowance so you’re not taxed on any returns. You can do this buy opening a Stocks and Shares ISA. Martin Lewis’s Money Saving Expert Blog does a brilliant job of giving you all the need to know info on where and how to start. I don’t think you’d gain anything from me regurgitating all that info.

I have been using Nutmeg (a JP Morgan company) for 5 years now, and Moneybox for about a year. My advice in choosing a platform would be to look at the best opening promotions and how you would like to manage your accounts. One of my annoyances with Moneybox has been that they only have an app, not a website.

If you’re interested in using Nutmeg please consider opening an account through my referral link!

Conclusion

Working in the age of the cost of living crisis is rough, no matter what industry you’re in or what job you’re doing. I personally don’t think salaries for skilled jobs (literally anything not minimum wage) are at all keeping up with minimum wage increases, let alone the national living wage. This means we’re pretty much all over-worked, under-payed and under-valued by our employers.

Don’t let this stop you having career ambition, and financial ambition. But do take this as a sign to not compare yourself to others, and to be kind to yourself. It is ok if you can’t save any money at the moment – I can’t! But that also doesn’t stop you from empowering yourself with knowledge on how you can better your financial situation in the future.

I hope if you got to the end of reading this that you gained something from it.

Disclaimer: I am not a financial advisor and this is not individualised financial advice. Please don’t sue me x

Leave a Reply